Asset Class Performance in 2023 and Looking Ahead to 2024

As 2023 enters the home stretch, we reflect on asset class performance so far in the year, and discuss what our models are saying for the next 12 months.

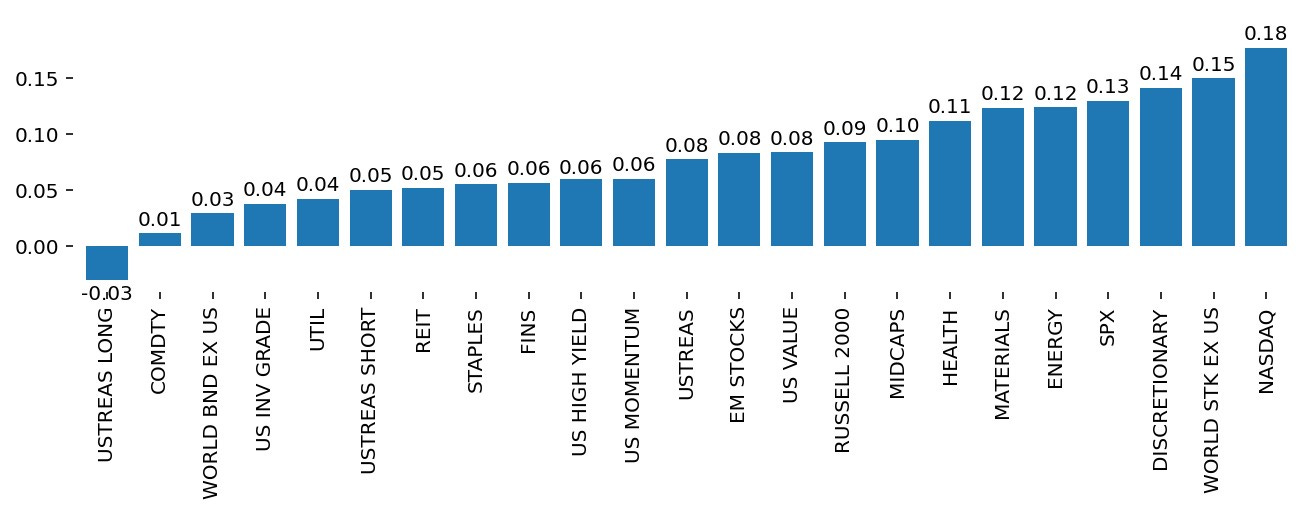

As the 3rd quarter earnings season gets under way, we look back at winners and losers so far this year. The next chart shows the 2023 year-to-date performance (orange bars) and the 2022 performance (blue bars) of a collection of asset classes. Asset classes are sorted from highest to lowest based on their performance so far in 2023.

The winners

The top performer in 2023 has been NASDAQ, up over 30% (as well as its high-flying cousin QQQ). The reasons are well known — excitement about AI and strong operating performance — but often overlooked is the fact that the move in 2023 has not even retraced the losses that NASDAQ experienced in 2022, and the index is still well off its highs from late-2021. Close behind NASDAQ is the consumer discretionary index (XLY), but given that over 40% of that index’s market capitalization consists of Amazon and Tesla, its performance is largely driven by the same set of considerations driving NASDAQ.

The overall stock market, as measured by the S&P 500, is having a good year, up roughly 15%, also largely driven by its sizable tech exposure. This holds internationally as well, as the MSCI All Country World Index (ACWI) and its ex-U.S. counterpart (VXUS) are up 12% and 8% respectively.

High-yield bonds have done well, despite the poor performance of most other fixed-income asset classes as rate rises that began in 2021 have continued into 2023.

High yield, which trades more on credit risk than interest rate risk, has been resilient, and without a sharp spike in default rates, the high carry from owning high yield bonds has propelled the asset class in 2023. Risk-parity strategies (SPRT15T) — which allocate equal risk to equities, bonds, and commodities — have eked out small gain in 2023 after a disastrous 2022.

Notable underperformers on the equity side are small-caps (Russell 2000) and midcaps. Despite having had very weak returns in 2022 and despite the 2023 rally in large-capitalization stocks, these have continued to be laggards, though they are up slightly on the year.

Rounding out the 2023 gainers, though with only small positive returns, are energy, commodities, and the U.S. dollar. For energy and commodities, constrained supply (some of it intentional due to OPEC policy) and stronger-than-expected economic growth have been the driving factors. Also contributing is the horrific terrorist attack perpetrated against Israel by Hamas on October 7th, which has raised fears of a wider Middle East conflict and led to higher oil prices. Faster-than-expected growth in the U.S. and the associated rate increases have led to dollar strength. Of the 2023 winners, only energy, commodities, and the dollar were also winners in 2022. All other 2023 gainers had negative returns in the prior year.

The losers

On the equity side, the biggest losers in 2023 have been utilities, REITS, and staples. Utilities are a high-dividend, bond-like asset class, and often trade in line with the Treasury market. The increase in rates has been very negative for utilities, propelling them into last place by performance among the major asset classes in 2023. Close to the bottom of the performance chart are REITs and staples (XLP). REITs are high-dividend, rate-sensitive stocks, a bad combination for performance so far this year. In addition, REITs are heavily exposed to commercial real-estate, which is suffering both from the post-COVID work-from-home trend and from tighter credit conditions among regional banks in the U.S. Staples, which are not heavily real-estate exposed and which benefit from a healthy U.S. consumer, have done poorly, perhaps because their high dividend yield makes them bond-like.

Medium-duration (labeled USTREAS and tradable via the VGIT ETF) and long-duration (labeled USTREAS LONG and tradable via the VGLT ETF) Treasuries have done poorly, as rates increased in 2023. Global sovereign bonds excluding U.S. dollar ones also did quite poorly, partially because rates increased, but also because of dollar appreciation (IGOV).

Financials have had a tough 2023 as the increase in the cost of deposits combined with their long-dated, low-coupon assets to create earnings issues for many banks and other financial firms, as well as solvency problems for some (like Silicon Valley and First Republic banks). Given the continued inversion of the yield curve, the business of borrowing short to lend long will not look attractive for the next 6-12 months.

Healthcare stocks are having another bad year in 2023, as they did in 2022, mostly on the back of Medicare price rules introduced in the Inflation Reduction Act. While the sector has attractive long-term prospects, in the short-run the going is likely to be challenging.

Interestingly, with the exception of utilities which saw a small gain in 2022, all of the 2023 losers were losers in 2022. Recent research has suggested that macro trends are pronounced in financial markets, and the last two years are a testament to this finding.

What comes next?

As we recently wrote, it is likely that interest rates will stop increasing. The crux of the argument is that the Fed and central banks globally have already introduced enough tightening to slow inflation, which is coming down in the U.S. and across most developed market economies. As inflation falls and growth slows, rates are likely to come down as well. Rate sensitive securities – like Treasuries, international bonds, and utilities – may thus benefit in the coming year. Second, we do not believe that tech stocks are in a bubble. The factors that contributed to tech stock and overall stock market strength – a strong consumer, the AI revolution, good earnings – are likely to continue into 2024. Furthermore, historically, stocks have done well in the year before the start of a Fed easing cycle, which is currently forecast to begin in late-2024 by Fed Funds Futures markets. The trends that have hurt REIT and bank performance – work-from-home and expensive deposits – are likely to stay in place damping these sectors’ performance. Finally, as we recently pointed out, oil inventories are tight and OPEC is suppressing production. Add to this a growing threat of a wider conflict in the Middle East, and the energy complex is likely to remain well bid.

Outside of these subjective considerations, at QuantStreet, we invest using a signal which combines our machine learning model’s return forecast with the last 12-month return trend of each asset class. The next chart shows our combined signals for 12-month ahead returns across our tracked asset classes (a subset of the performance chart shown above). Our forward-looking return rankings across asset classes reflect lagged asset class performance, but are tempered by the machine learning model’s forecast. For example, some of the 2023 losers look attractive based on our return forecasting model, so their signal turns out to be positive, despite highly negative 2023 returns. The 2023 winners sometimes look less attractive in the combined signal because their positive trend is offset by a weak model forecast.

Importantly, these signal rankings alone are not enough for optimal portfolio formation. Investors should also consider how risky each asset class is and how asset-class returns are correlated with one another. Using such risk information, the output from our signals shown above, as well as an understanding of their own risk preferences and liquidity needs, investors can construct optimal portfolios that reflect these disparate influences. This is something QuantStreet does for our clients, but that is a story for another day.

Key to returns figure

The names of the indexes shown in the returns figure are: