Don't Fight the Fed: What Happens When the Fed Begins to Ease?

Futures markets are forecasting a Fed rate cut sometime in 2024. The Fed typically starts to ease ahead of economic weakness. But this isn't necessarily bad news for financial markets.

As of late-August 2023, the Fed Funds futures market is anticipating that the Federal Reserve will start cutting its policy rate sometime by mid-2024. In fact, the futures market anticipates almost 100 basis points (bps) of policy easing (i.e., lowering rates) by December of 2024.

As we show below, the Fed typically starts to ease monetary policy just ahead of weakening economic data. If the futures market is correct, we can expect that by the middle of next year, media forecasts of impending recession will be pervasive. Alongside these will be the inevitable forecasts of the negative impact of recessions on stock prices.

In anticipation of this gloomy narrative, we look at what actually happened in past episodes of Fed monetary policy easing. Our methodology is to identify the starts of past periods of Fed monetary policy easing, and then to analyze macroeconomic and financial market outcomes during these periods. The outcomes under consideration are: year-over-year changes in industrial production, the unemployment rate, inflation, the two-year Treasury yield, the returns of the S&P 500 index, and the behavior of S&P 500 earnings and price-to-earnings (P/E) ratios.

Past Easing Episodes

The next chart — which tracks the Fed Funds rate — shows the 11 policy easing cycles that out algorithm identified over the last 50 years. In a typical easing episode, the Fed lowers the Fed Funds target rate to stave off slowing growth and rising unemployment. The general contours of Fed monetary policy consist of very high rates in the late-1970s to fight against the inflationary pressures set off by the 1973 oil crisis, followed by a lower-rate regime from 1990 until today. The early-2000s, late-2000s, and 2020 rate cutting cycles were preceded by the bursting of the dot-com bubble in 2000, the Global Financial Crisis of 2008-2009, and the onset of the COVID-19 pandemic.

In our classification scheme, a financial easing episode begins with a cut to the Fed Funds target rate after it has been unchanged in the prior month-over-month period. The total amount of easing needs to exceed 150 basis points over the next two years, and the policy rate must be below its starting point throughout this two-year period. Based on this classification rule, the following figure zooms in on the behavior of the Fed Funds rate in the six months before and after the start of Fed monetary policy easing.

The next chart shows the behavior of year-over-year changes in industrial production (IP YoY) heading into and after the start of Fed easing episodes. The dark blue line shows the average IP YoY across all 11 Fed easing episodes identified in the above analysis, with the blue shaded area representing the degree of uncertainty around the average IP YoY response.

In the year before the start of Fed easing, IP YoY begins to decline, and continues to decline in the year after the start of policy easing, reaching a nadir of -2.5%. At this point, industrial production growth begins to pick up and the year-over-year growth in industrial production two years after the start of the easing episode is, on average, close to 5%.

The U.S. unemployment rate stays largely flat in the month in which easing episodes begin, but quickly accelerates and is, on average, about 2% higher a year into an easing episode than at the episode’s start. Following this peak, the unemployment rate begins to slowly decline, though even two years after the beginning of easing episodes, the unemployment rate remains elevated.

Finally, CPI inflation heading into Fed policy easing is typically flat, but then inflation declines rapidly once easing starts, and begin to slowly recover back to the pre-easing level around 20 months after the start of the easing policy. Year-over-year CPI inflation remains well below its pre-easing level even two years after the start of the looser monetary policy regime.

The three figures above demonstrate that the Fed begins to ease ahead of weakening economic conditions and lower inflation, in line with its dual policy mandate of maintaining price stability and full employment. Importantly, the causality in the above figures runs from the Fed’s anticipation of weakening economic conditions to the Fed’s policy response: In an effort to spur more robust economic activity, the Fed eases monetary policy because it anticipates slower growth.

Market Responses

The next figure shows that monetary policy easing episodes are associated with sharply falling short-term Treasury yields. The two-year Treasury yield falls an average of close to 300 basis points in the two-year period following the start of easing episodes, though the magnitude of this drop is heavily influenced by the easing events which took place in the high-interest rate environment of the 1970s.

The next figure shows that, despite slower economic growth, the S&P 500 index still manages to eke out a healthy 30% return in the two-year period following the start of a Fed easing cycle. This is surprising since we just showed that economic growth slows, and one may imagine this is an adverse environment for the stock market. We explore the reasons for this robust S&P 500 performance momentarily.

Another interesting aspect of this chart is that, according to the Fed Funds futures market, the start of the current easing cycle will be around May of 2024. This puts us roughly at month -9 before the start of the easing cycle. And S&P 500 performance from month -9 to month 0 has historically been positive.

The following figure shows that there is substantial variation in S&P 500 behavior post-Fed easing episodes. Each panel shows the behavior of the S&P 500 index in the two years before and after the start of each easing cycle. Each episode is labeled with the month prior to the first Fed rate cut. Outside of the easing episodes that start in December 2000 and August 2007 (the months before the first rate cut), where the stock market experienced steep declines, all other easing episodes are associated with strong stock market returns. While the average S&P 500 return of 30% hides much of this variation, the central message that stocks typically do well following easing episodes carries through.

The Mechanism

To better understand the mechanism underlying the stock market’s strong performance in difficult macroeconomic conditions, we first examine the behavior of corporate earnings around the starts of Fed easing cycles. As the next figure shows, S&P 500 earnings per share rise going into easing cycles, but then fall by around 10%, before rebounding a bit by the end of the two-year post-easing period.

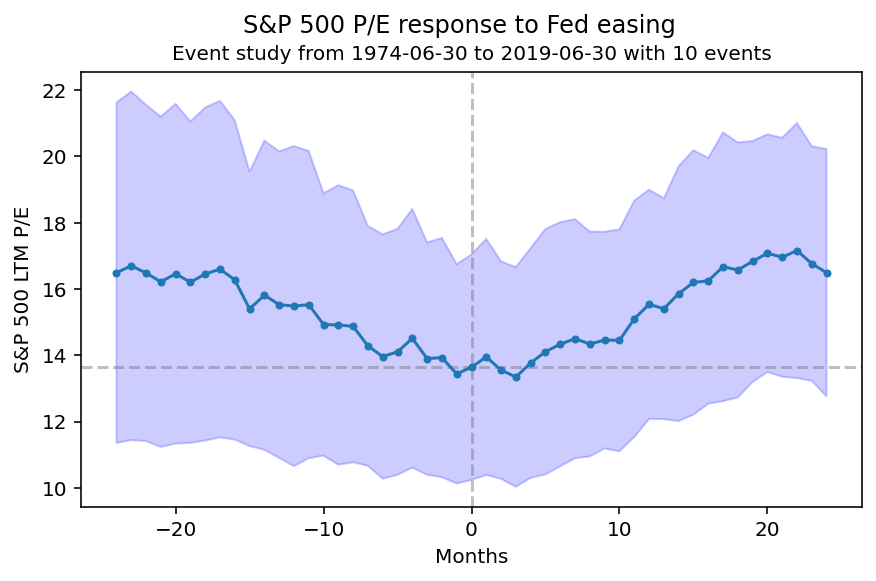

While this earnings behavior is consistent with the economic slowdown we already documented, consider what happens to stock valuation multiples during easing episodes. The average S&P 500 price-to-earnings (P/E) ratio falls from around 16.5 to just under 14 by the start of an easing cycle. But once easing starts, P/E ratios bounce in the subsequent two years by roughly 2.5 turns to a high of around 17 by month 22 after the start of the easing cycle. (Note that these multiples reflect some easing episodes during the 1970s when interest rates where in the mid-teens and when P/E ratios were considerably lower than today.)

This bounce in valuations means that the drop in interest rates associated with Fed easing cycles leads to lower discount rates applied to future corporate cash flows which raises price levels relative to current earnings levels, i.e., P/E ratios go up. Despite the weaker economic growth and weaker corporate earnings in the aftermath of the start of Fed easing cycles, the valuation effect dominates and the increase in multiples has historically been enough to lead to increasing stock prices in the two-year period after the start of Fed easing.

Takeaways

If the Fed Funds futures market is making a correct forecast, and if the historical pattern of Fed easing ahead of a slowdown in economic growth materializes, then we can anticipate the start of weaker economic conditions and policy easing sometime in mid-2024. Historically, S&P 500 returns from the current point in the monetary cycle until the start of easing have been positive.

Following the start of easing, economic growth is likely to slow, unemployment is likely to rise, and inflation is likely to be tame. At the same time, short-term interest rates are likely to fall starting in mid-2024 and corporate earnings growth will slow. However, price-to-earnings ratios are likely to increase on the back of falling discount rates brought about by easing monetary policy, the net effect of which will be to lift stock prices.

Of course, things may play out quite differently than the average outcomes over past easing cycles. Some easing cycles, e.g., the ones that began in early-2001 and 2007, were followed by large stock market declines. Investors should consider these risks and position their portfolios in line with their risk tolerance and liquidity needs. Those who are uncertain how to proceed should consult with a qualified financial advisor.