Healthcare Stocks: Fundamentals vs. Inflation and Regulation

Healthcare stocks have been market laggards on the back of cost pressures and punitive regulations. However, the long-term trends are extremely favorable making the sector an interesting opportunity.

Healthcare stocks have performed largely in line with the S&P 500 index over the last ten years. The next figure shows the performance of XLV, the Healthcare SPDR exchange traded fund (ETF), and the S&P 500 index since 2013, with both indexes normalized to start at 100.

However, over the last year, the S&P 500 has seen a large outperformance relative to XLV, as the next chart shows (both indexes are normalized to 100 at the start of the chart).

There are multiple reasons for the S&P 500 outperformance. One contributor has been investor enthusiasm about artificial intelligence (AI) and the consequent large rally in technology stocks, which are heavily represented in the S&P 500 index. On the other hand, healthcare firms have been particularly hard hit by inflation and labor cost pressures. A further headwind has been an adverse regulatory landscape for healthcare firms.

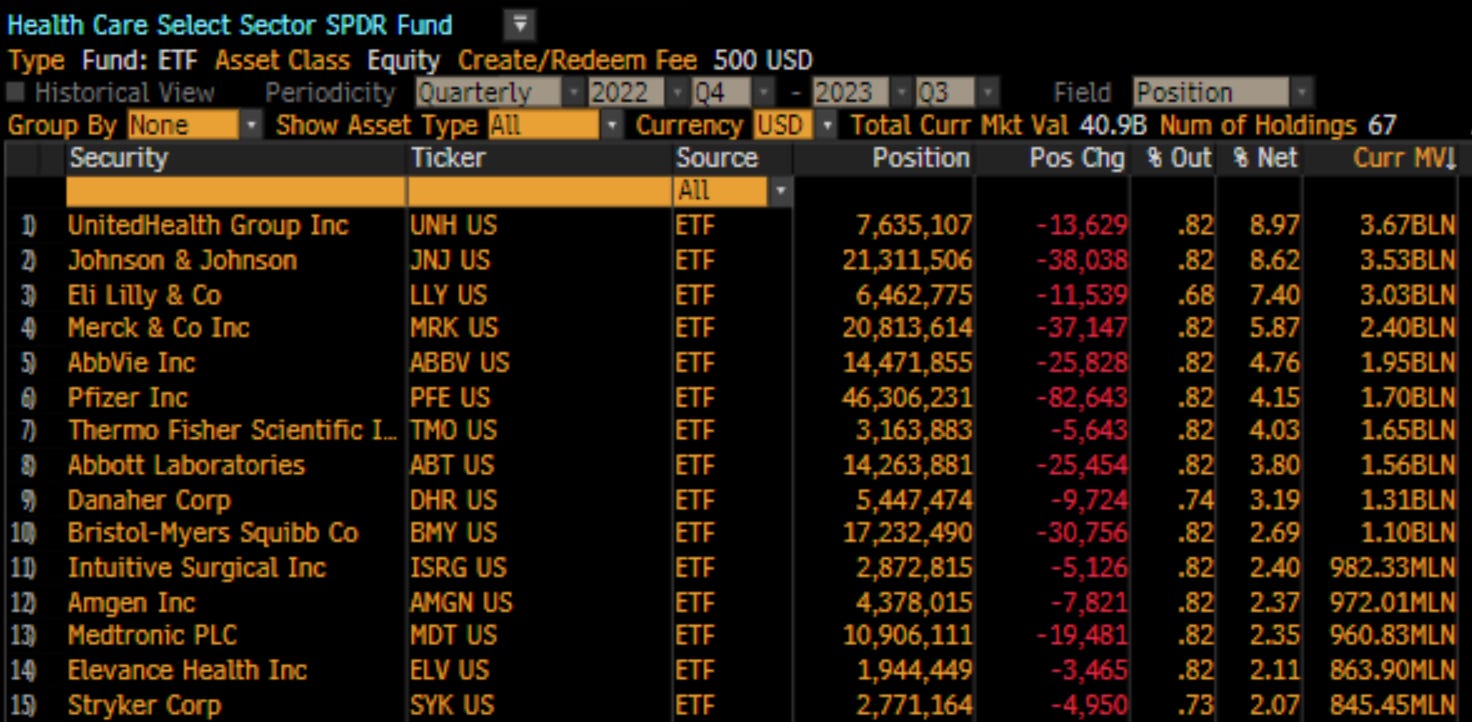

The next table shows the composition of the XLV ETF. The firms are shown starting with the largest component of XLV (UnitedHealth) at the top, with the next largest (Johnson & Johnson) in the second row, and so on.

With the exception of UnitedHealth, a health insurance and benefits company, all the largest components of the XLV are involved in drug or medical device development. AI and other analytics innovations, which have spurred so much enthusiasm in the tech stocks space, will also benefit these firms. Demographic trends are firmly supportive of the entire healthcare sector. The question is whether these positive fundamentals are enough to offset inflation and regulatory headwinds.

Inflation and Regulation

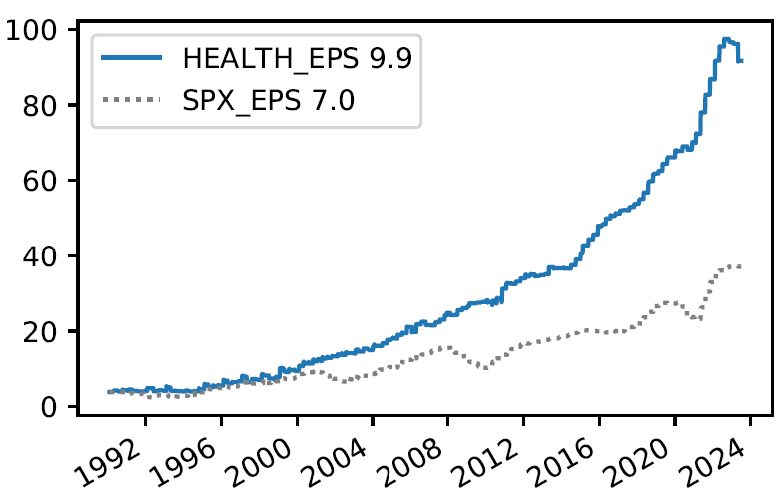

Healthcare sector earnings growth has outpaced that of the broad S&P 500 index over the last three decades. Healthcare earnings-per-share (EPS) has grown at a compound annual growth rate of 9.9% versus 7% for the S&P 500 index.

However, over the past year, healthcare EPS growth has lagged that of the broader market. Part of this is due to price pressures and labor shortages according to a recent McKinsey report. While these trends are unlikely to disappear in the near-term, a Fed which is very focused on taming inflation and a labor market that will naturally adjust mean that these pressures will abate. The McKinsey report concludes that:

The US healthcare industry faces demanding conditions in 2023, including recessionary pressure, continuing high inflation rates, labor shortages, and endemic COVID-19. But players are not standing still. We expect accelerated improvement efforts to help the industry address these challenges in 2024 and beyond, leading to an eventual return to historical average profit margins.

The industry is also facing headwinds on the regulatory front. The Inflation Reduction Act (IRA) was signed into law on August 16, 2022. This new legislation gives Medicare unprecedented power to negotiate prices with drug manufacturers and then to punish those firms that do not comply with the mandates handed down by the Department of Health and Human Services. Unsurprisingly, the power to punish non-compliance has met with fierce industry resistance. Merck recently sued the US government (Wall Street Journal article) arguing that the structure of the IRA is unconstitutional. Time will tell how the regulatory landscape evolves, but given the pro-business predisposition of the present Supreme Court, and the likelihood (according to the above Wall Street Journal article) that this case ends up there, there is a not insignificant chance that some of the present regulatory pressures will abate.

Artificial Intelligence in Medicine

While the immediate impact of AI in medicine is likely more on the efficiency side (like auto-generation of patient meeting summaries), the medium- and long-term impacts from AI and technological innovation more broadly will be considerably more far-reaching. An example of the attention that computational methods are receiving in biology can be seen anecdotally (for example, the Center for Computational Biology at the Flatiron Institute) and systematically (do a search on Google Scholar for computational biology articles so far in 2023). With regard to the impact of technology on medicine, the New York Times Magazine claims in a recent article that:

We may be on the cusp of an era of astonishing innovation — the limits of which aren’t even clear yet.

Technological innovation does not necessarily translate into stock market returns, but given the underlying science, if investors have become excited about the impact of AI on growth prospects of technology firms, they may well become excited about the growth impacts of the same technologies in the healthcare space. This shift in investor focus hasn’t yet occurred, but the ingredients for it are in place.

Demographics

According to global demographic projections, the share of elderly in the world’s population is set to steadily rise over the rest of the 21st century. According to the Our World in Data project, the fastest growing demographic group over the remainder of the century will be the 65+ cohort, and the second-fastest growing group will be the 25-64 year-old one.

While the are innumerable issues about how a globally-aging population — much of it from developing countries — will be able to afford expensive, developed country medical treatments, the underlying increase in demand for all manner of healthcare is likely to be an industry tailwind for decades to come.

Valuations

The healthcare sector faces near-term headwinds in the form of inflation and wage pressures, medium-term headwinds in the form of an increased regulatory burden, but long-term tailwinds due to favorable demographics and the rapid pace of technological innovation.

On the valuation front, the price-to-book (P/B) ratio of the the healthcare sector has traditionally traded above the P/B ratio of the overall market, though now the valuation gap has closed substantially.

Another take on the valuation picture is to look at the earning-yield (earnings-to-price ratio) of the healthcare sector relative to the level of 10-year Treasury rates. Based on this metric (EPRF), the healthcare sector is also “cheap” relative to the market overall, as its earnings yield is a few percentage points higher than that of the overall market, even though both measures tend to track each other quite closely over time.

While these valuation arguments are suggestive, a more rigorous look at how current fundamentals and valuations impact expected returns of healthcare stocks requires a model-based approach. At QuantStreet, we have two models that allow us to assess the future return prospects of the healthcare (and other) sectors.

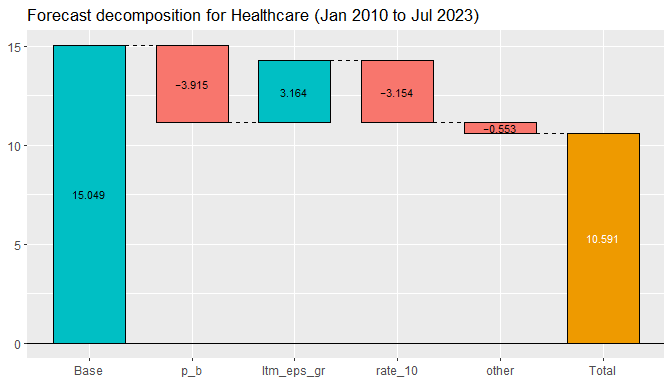

One of the models looks at how US sector-level year-ahead returns have historically responded to different forecasting variables. The next figure shows the forecast coming from this model for the healthcare sector.

The first bar (Base) gives the return forecast for the sector if all forecasting variables are equal to their average values in the interval over which we estimated the model. The next bar (p_b) shows that the current, relatively high price-to-book ratio of the sector decreases the return estimate by 3.92%. On the other hand, the dip in past earnings growth (ltm_eps_gr) actually contributes a positive 3.16% to the return forecast because of the historical association between lower growth rates and higher future returns (perhaps because sectors with slow growth in a given year tend to get overly penalized by the market). The currently high level of 10-year US Treasury interest rates contributes a negative 3.15%. Other forecasting variables have a minimal impact. The net forecast is for a +10.59% next-year return.

We have a second forecasting model which uses machine learning techniques to repeat this analysis at the level of individual asset classes, and this model generates a similar +10.74% year-ahead forecast. Interestingly, the second model raises the baseline forecast due to slower, lagged earnings growth and reduces the forecast due to relatively high current valuations, measured via a low earning-yield relative to 10-year Treasury rate (EPRF). Overall the two models offer very similar forecasts, and for similar reasons.

Summary

The healthcare sector offers a compelling investment opportunity based on long-term fundamental prospects and attractive current valuations. The problem with this thesis is timing. The industry positives — technological innovation and demographics — are multi-year or multi-decade trends. The regulatory burden will be negative for the sector in the medium-term, if not for longer. Inflation and labor market pressures are issues right now. In our view, the positives will win out eventually and make the healthcare sector an important component of investor strategic portfolios. But, from a tactical point of view, it is impossible to say when the long-term positive trends will outweigh the shorter-term negatives.

As always, investors should position their portfolios to take into account their risk preferences and liquidity needs. Those who feel they don’t have the information to make informed decisions should consult with a qualified investment advisor.